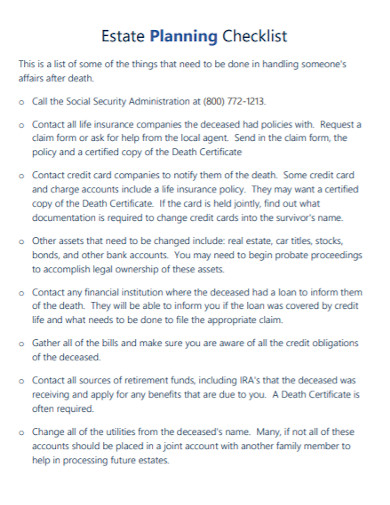

Estate planning entails deciding how a person’s assets will be kept, administered, and distributed after their death. It also considers how an individual’s property and financial responsibilities will be managed in the occasion that they become disabled. Houses, automobiles, stocks, artwork, life insurance, pensions, and debt are some of the assets that might help compensate an individual’s estate. Estate planning serves a variety of purposes, including protecting family wealth, supporting for a surviving spouse and children, supporting children’s or grandchildren’s schooling, and leaving a charity legacy.

10+ Estate Planning Checklist Samples

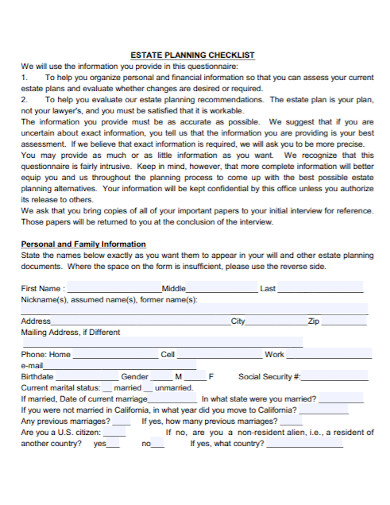

Making the proper preparations so that everything you possess, or “estate,” goes to the appropriate person when you die is known as estate planning. Land assets, vehicles, banking information, investments and insurance, furniture, jewelry, and other valuables may all be included in an estate. Estate planning is the process of preparing duties to handle a person’s assets in the event of disablement or death. The gift of possessions to heirs and the settlement of inheritance taxes are all part of the preparation. Most estate plans are developed with the assistance of an estate law practitioner.

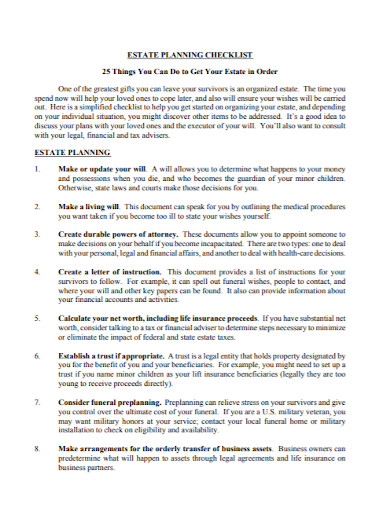

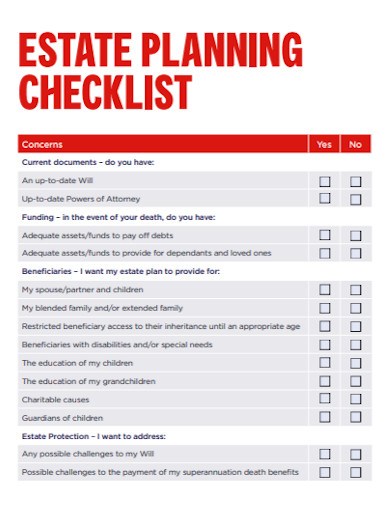

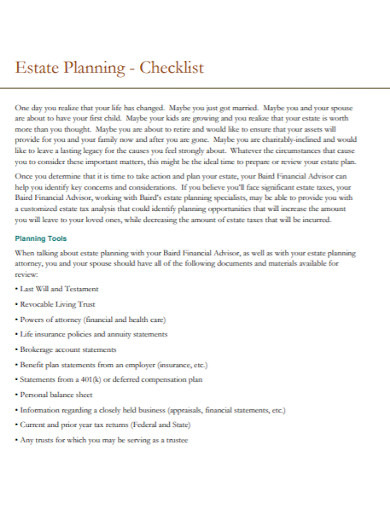

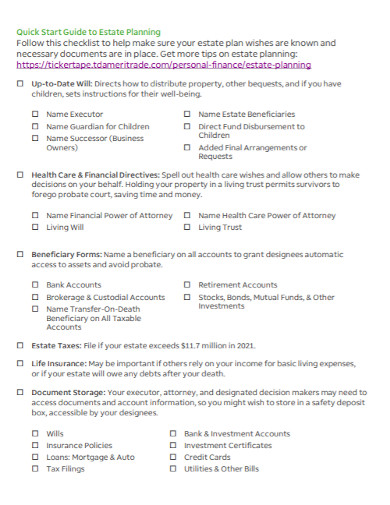

1. Estate Planning Checklist Template

2. Standard Estate Planning Checklist

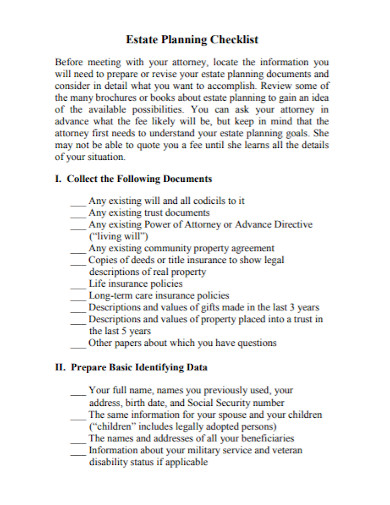

3. Basic Estate Planning Checklist

4. Estate Planning Checklist in PDF

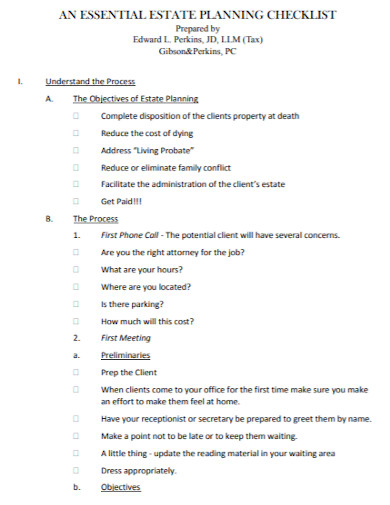

5. Essential Estate Planning Checklist

6. Printable Estate Planning Checklist

7. Professional Estate Planning Checklist

8. General Estate Planning Checklist

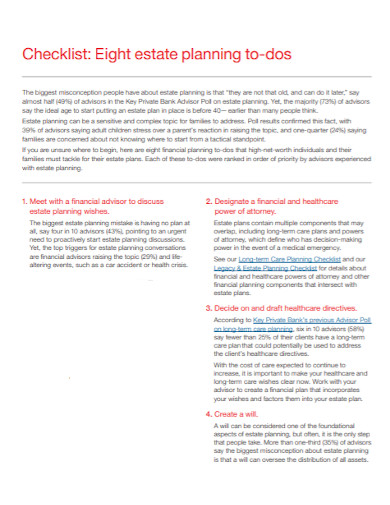

9. Eight Estate Planning Checklist

10. Estate Planning Checklist List

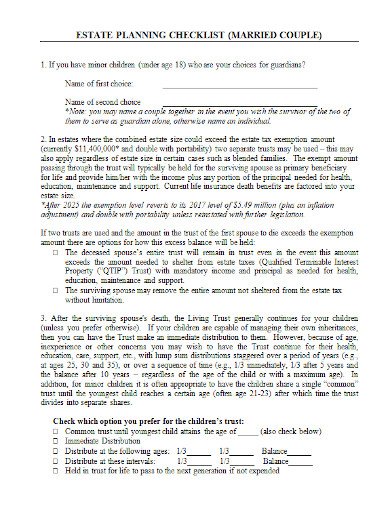

11. Couple Estate Planning Checklist

Writing a Will

A will is a legal document that specifies how an individual’s property and, if applicable, custody of minor children must be administered after death. The document describes the individual’s preferences and specifies a trustee or executor whom they trust to carry out their real intent. The will also specifies whether a trust should be established following the death of the testator. A trust can be established during the estate owner’s lifetime (living trust) or after their passing (deed trust) (testamentary trust).

A legal process called as probate is used to examine the accuracy of a will. The first stage in managing a deceased person’s estate and allocating assets to dependents is probate. When a person dies, the will’s custodian must deliver the will to the probate court or the executor appointed in the will inside of 30 days of the testator’s death.

The probate process is a court-supervised method in which the validity of the deceased’s will is established and recognized as his or her true last testament. The executor listed in the will is legally appointed by the court, which grants the executor legal authority to act on behalf of the departed.

Estate Freezing

Another way to reduce death taxes is to employ this method. It entails an individual locking in the existing worth of their property, and hence their tax payable, while allocating the value of future development to another person. Any future growth in the value of the assets is passed to the advantage of someone else, such as a spouse, kid, or grandchild.

The value of an asset is frozen at its value on the day of transfer using this method. As a result, the amount of possible capital gain at death is likewise frozen, enabling the estate planner to anticipate their prospective tax burden and good system for income tax payment.

FAQs

What is a life insurance?

Life insurance is used to pay death taxes and fees, as well as to fund corporate buy-sell agreements and retirement plans. Any income tax on deemed disposal of assets upon an individual’s death can be paid without selling assets if adequate insurance proceeds are available and the policies are appropriately arranged. The proceeds of life insurance received by the beneficiaries upon the insured’s death are normally tax-free.

What other strategy an estate planner can take?

Giving to charitable organizations while living is another approach an estate planner might use to reduce the estate’s tax liability after death. Because the donations are not included in the taxable estate, they diminish the estate’s financial size, cutting the estate tax liability.

Because estate planning is a complicated and time-consuming procedure, it is better to enlist the assistance of another individual. A paid lawyer, a skilled financial advisor, or a trusted friend who can assist you with the development, paperwork, and execution of your will could have been that person.

Related Posts

FREE 18+ Complaint Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Internship Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Statement Checklist Samples in MS Word | Google Sheets | PDF

FREE 20+ Voluntary Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Summary Checklist Samples in MS Word | Google Sheets | PDF

FREE 14+ Sponsorship Checklist Samples in MS Word | MS Excel | PDF

FREE 18+ Conference Checklist Samples in MS Word | Google Sheets | PDF

FREE 17+ Lesson Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Progress Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Enrollment Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Graduation Checklist Samples in MS Word | Google Sheets | PDF

FREE 15+ Consent Checklist Samples in MS Word | Google Sheets | PDF

FREE 18+ Review Checklist Samples in MS Word | Apple Pages | PDF

FREE 18+ Submission Checklist Samples in MS Word | Google Docs | PDF

FREE 18+ Request Checklist Samples in MS Word | MS Excel | PDF