It is a common occurrence that an individual receives a phone call or a legal notice from a collection company that is looking for payments. Once a debt collector reaches out to you in relevance to an unpaid event, your first plan of action is to require a debt validation letter. This is to make sure and confirm that the debt belongs to you before paying the collector. It is one of the collector’s roles and responsibilities to provide you with a debt validation letter that contains an outline of what the debt is, how much is owed, and the deadline it needs to be paid.

15+ Debt Validation Letter Samples

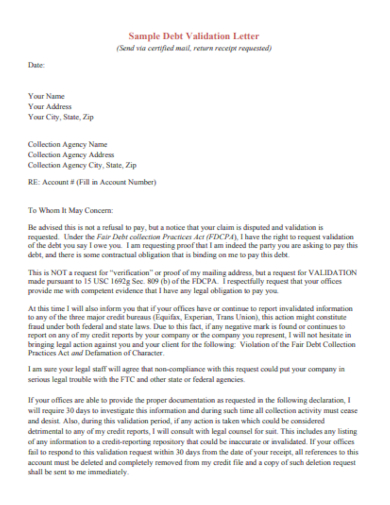

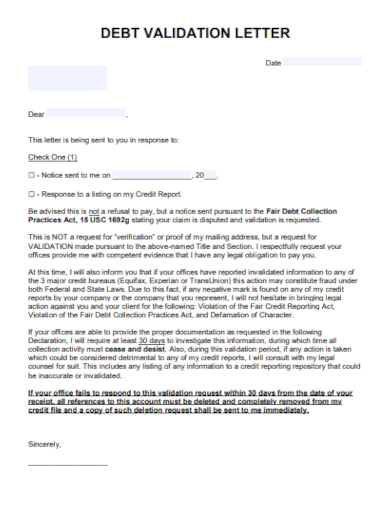

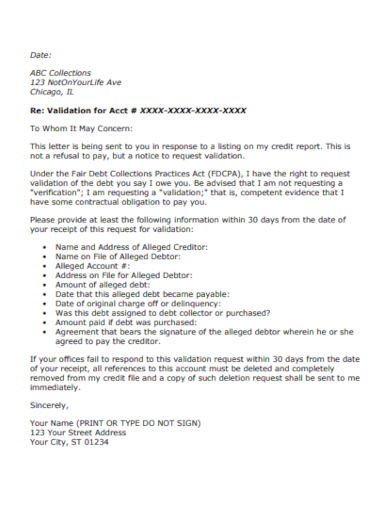

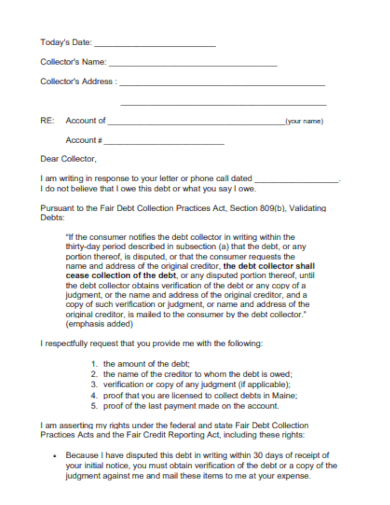

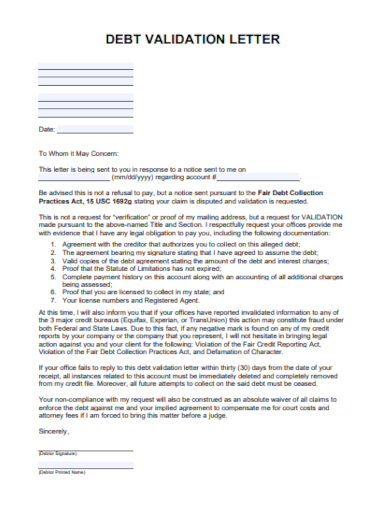

1. Debt Validation Letter Template

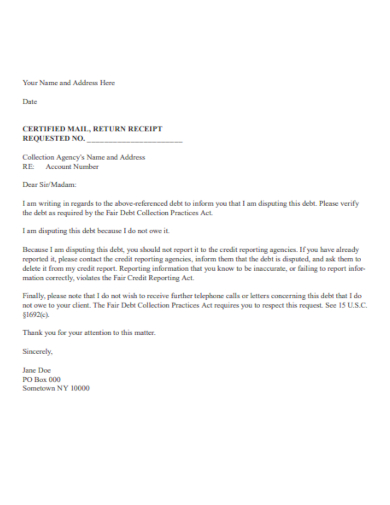

2. Sample Debt Validation Letter

3. Free Debt Validation Letter

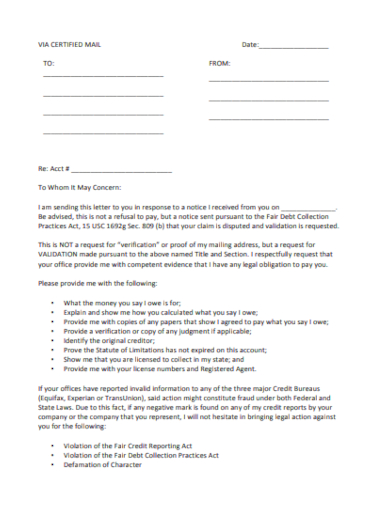

4. Request for Debt Validation Letter

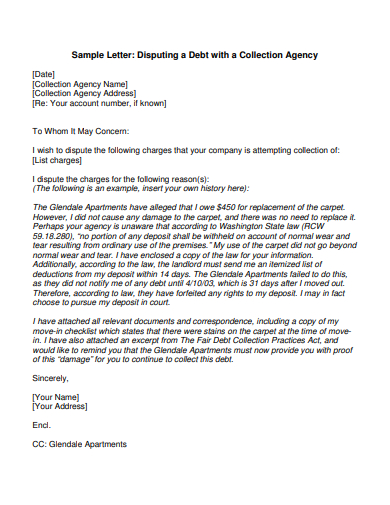

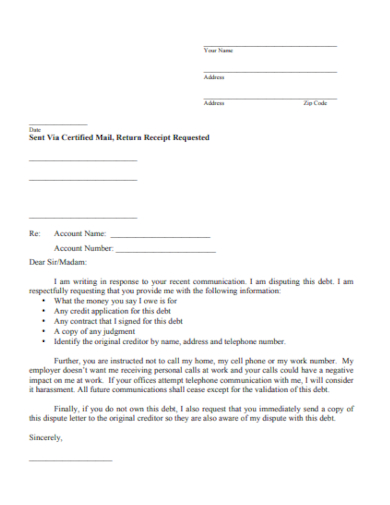

5. Debt Collection Dispute Letter

6. Standard Debt Validation Letter

7. Agency Debt Validation Letter

8. Downloadable Debt Validation Letter

9. Certified Debt Validation Letter

10. Formal Debt Validation Letter

11. Debt Dispute Validation Letter

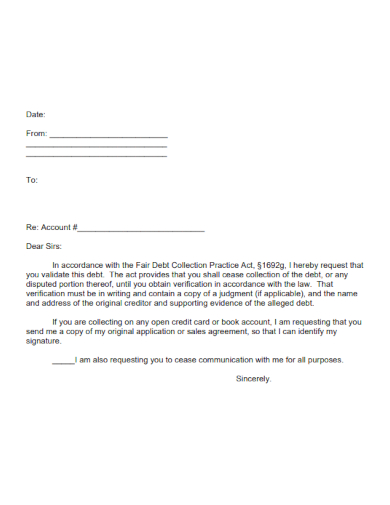

12. Debt Validation Letter Format

13. Debt Dispute Validation Request Letter

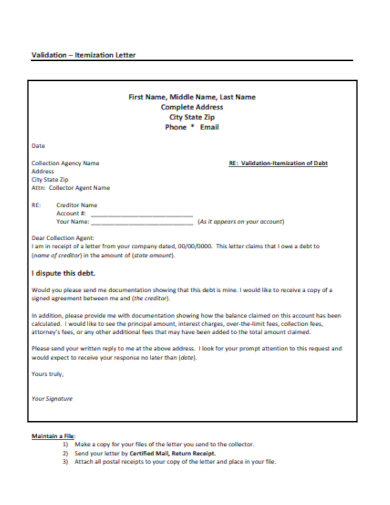

14. Debt Validation Itemization Letter

15. Follow-Up Debt Validation Letter

16. Initial Debt Validation Letter

What is a Debt Validation Letter?

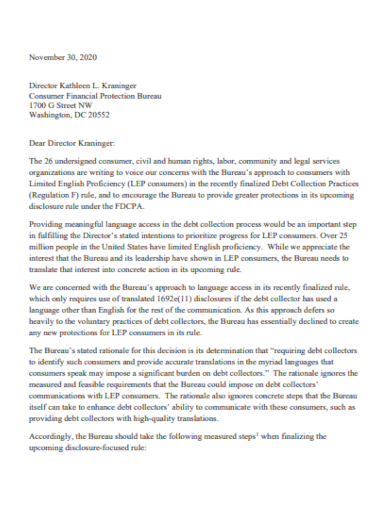

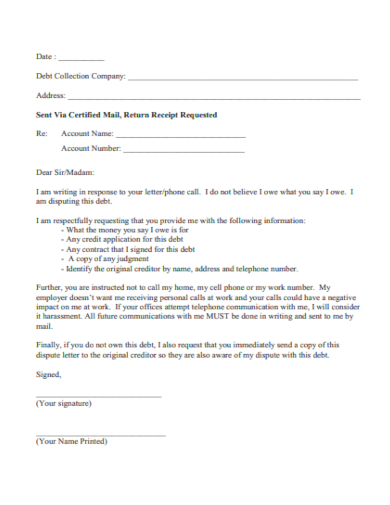

Debt validation letters are one of the important legal and formal letters required during a debt collection process. This letter helps an individual in confirming if they have an existing debt and prevents them from paying a debt that does not belong to them. A debt validation letter also contains information on how much a person owes and to who, as well as the extra fees or interest rates the collector has included. Other relevant documents and templates you can use includes the collection letter, settlement offer letter, credit dispute letter, demand letter, informal debt agreement, agreement letter, and cease and desist letter.

How to Send a Debt Validation Letter

A debt validation letter is an effective way to confirm if you have an existing debt or not. A consumer writes and sends this letter to a collection agency when they receive a letter that contains a request for payment for a particular unpaid balance. According to federal law, collection agencies are required to give information about the balance given that the debtor provides a verification letter within 30 days of the initial contact or communication.

Step 1: Check When the Collector’s Initial Contact

The debtor has thirty days to provide a debt validation letter from the day they received a request for payment from a collection agency which is also called the ‘initial contact’. This communication can be in a form of a phone call or mailed notice.

Step 2: Write Your Debt Validation Letter

A debt validation letter aims to inform the collection agency that the consumer or debtor is aware of their FDCPA rights and is requesting other relevant information to prove that the debt is theirs to pay and is accurate.

Step 3: Provide Your Signature Then Send the Document

After completing your letter, provide your signature above your printed name. It might not be one of the legal requirements but it provides a level of authenticity to the document. Bring your letter to a nearby post office and sent it through “Certified Mail with Signature Confirmation”.

Step 4: Wait for the Response

Once the debt validation letter is received by the creditor, they have 30 days to provide their response. If they have not provided the necessary response within the given timeframe, the debt will be considered invalid according to federal law and the debtor can move forward without paying the said debt. If the collection agency did respond, the debtor must proceed to all provided documentation to search for points in which the case has been incorrectly assigned. If proven that the debt is valid, the debtor can start making payments.

FAQs

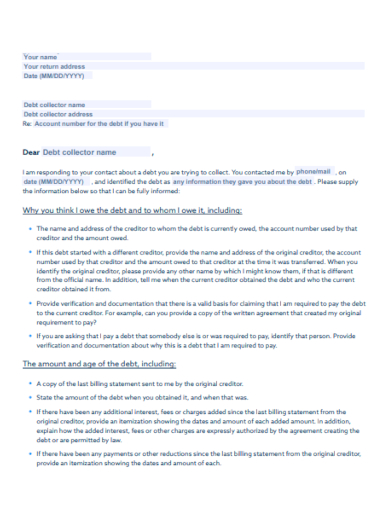

What information should be included in the debt validation letter?

A debt validation letter must contain the debtor’s name and address, the collection agency’s name and address, acknowledgment of the contract, a statement that expresses dispute to the debt, a request for proof, a request for all details about the debt, contact information, and request to stop communication if the debt is not valid.

What is the difference between debt verification and debt validation letters?

Debt verification letters are sent by a consumer to request information about a certain debt while debt validation letters are sent by collection agencies to show that a debt exists and the consumer is responsible for paying it.

What is the purpose of a debt verification letter?

A debt verification letter helps you in determining the exact amount of your debt, collect documents to verify your debt, acquire information on who you owe, identify how old your debt is, and place a pause on the collection process.

Debt validation letters are sent to consumers by debt collectors or collection agencies to provide a formal request that the collector validates a particular debt they are trying to collect. This allows the consumer to perform their rights before paying the debt they are not sure belongs to them. This letter contains how much debt a consumer owes, the name of the creditor, the method on how to request information about the original creditor, and the right of the consumer to dispute the debt.

Related Posts

FREE 6+ Final Notice Letter Templates in PDF MS Word

FREE 8+ Sample Letter of Recommendation For Scholarship in MS ...

FREE 8+ Debt Management Plan Samples in PDF DOC

FREE 41+ Demand Letter Samples in PDF Google Docs | Pages ...

FREE 10+ Debt Settlement Agreement Samples [ Collection ...

FREE 10+ Debt Tracker Samples in PDF

FREE 45+ Examples of Authorization Letter Templates in PDF MS ...

FREE 10+ Collateralized Debt Obligation Samples in PDF

FREE 47+ Demand Letter Templates in PDF MS Word

FREE 119+ Letter Samples in PDF MS Word

FREE 99+ Simple Letter Templates in PDF MS Word

FREE 9+ Sample Financial Hardship Letter Templates in PDF MS ...

FREE 50+ Demand Letter Templates in PDF MS Word

FREE 7+ Cease and Desist Samples in PDF MS Word

FREE 105+ Letter Samples in PDF MS Word