A formal management audit committee does not exist on the board of directors of a corporation. Rather, board members sit on the remuneration committee and evaluate individual executives’ productivity based on quantitative data (organic profits, EBIT margins, segment margins, running cash flows, and EPS) as well as undefinable or intangible factors (e.g., efforts toward acquisition integration). A management audit will be conducted by an independent consultant hired by the board of directors. Although the audit’s scope may be limited, it is usually extensive, covering many important parts of a management team’s obligations.

10+ Management Audit Samples

A management audit is an evaluation of an organization’s management team’s competencies. The purpose of the analysis is to see how successfully this group can accomplish the company’s goals. Technical and operational planning, decision-making, financial and operational performance, and risk management may all be part of the audit. An independent third party normally conducts this type of audit. When the board of directors is considering a management change or a company realignment, they may request a management audit. When buying a business, an acquirer may conduct a management audit to see if any changes to the management team are necessary.

1. Management Audit

2. Quality Management Audit

3. Access Management Audit

4. Assets Management Audit

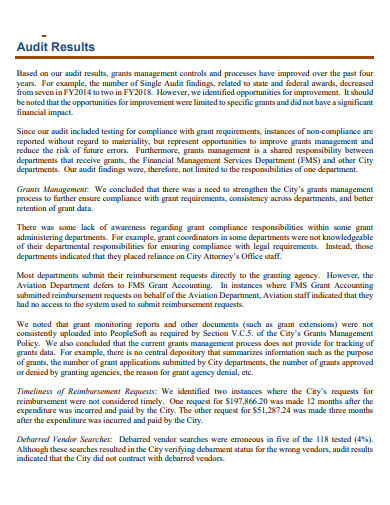

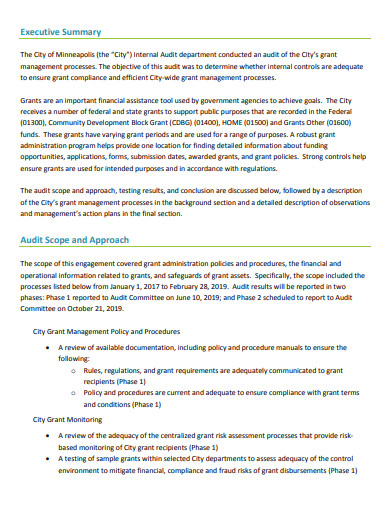

5. Grant Management Audit

6. Prudent and Economical Management Audit

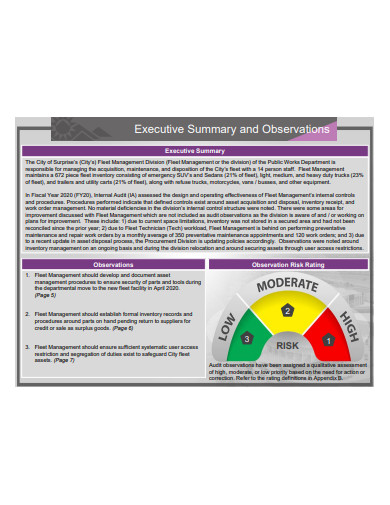

7. Fleet Management Internal Audit Report

8. Sample Grant Management Audit

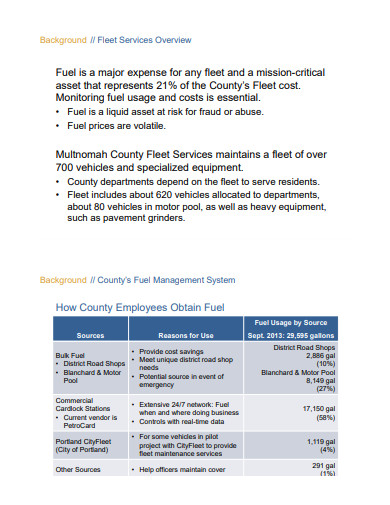

9. Fuel Management Audit

10. Project Management Audit

11. Management Audit Checklist

Implementing a Management Audit

A management audit’s purpose is to identify the management team’s flaws. The audit is usually done on a company-wide level, but it can also be done on a segment-by-segment basis. The idea is to always show how important management is and where improvements can be made.

Human resources, marketing, research and development (R&D), budgeting, management, financing, information technology, and business system are just a few of the areas that a management audit will look into.

Discussions with management and staff, financial report and performance assessment, a review of a company’s policies and procedures, an examination of training courses, the selection procedure, and many other aspects of an organization’s operations will all be part of the management audit.

When the audit is finished, the external audit firm will not only present its observations, but will also usually provide a whole strategy for the board of directors to adopt so that the company may run at peak efficiency.

In opposed to an internal audit, which is performed by a company’s internal audit department, a management audit is performed by outside businesses with specific expertise. Management audits are performed by well-known firms such as McKinsey & Company, Bain & Company, and the Boston Consulting Group.

A management audit could take weeks or months, based on the extent of the exercise. The audit report would seem like a report card, with high scores in areas where the management team succeeds and lower ratings in areas where changes are needed. In the very same way that the management team operates the company, the board would review these proposals and enforce modifications where appropriate.

FAQs

Why are audits important?

Audits give useful data. All impacted parties must be aware of the presence and application of product, process, and system controls, as well as whether or not these controls are effective. A report is produced after an auditor examines the controls against the requirements. When controls are in place and working, everyone’s faith in the process grows. If controls are missing or malfunctioning, resources can be used to correct the problem.

Why do you have to use facts to form conclusions?

Auditing is based on facts, with conclusions taken from the evidence. Facts can be excellent (a requirement was met) or bad (a criterion was not met), but they should not be tainted by judgment or opinion. These facts, sometimes referred to as objective evidence, can come from five different places. Physical qualities such as flow rates and dimensions; sensory-derived input such as seeing, hearing, smelling, or tasting; documents or records; information gleaned from auditee staff interviews; or patterns such as percentages or ratios Auditors determine the facts to be gathered using checklists and other methods, and then do fieldwork to gather these data.

Management audits necessitate some extra effort. The auditor must determine the level of discomfort connected with those groups of negative facts. (It’s critical to recognize business problems as pain, such as scrap, rework, and overtime.) The auditor then merges the lacking control (the system error producing the difficulties) and the business pain into a single statement, known as a finding. The discovery will disclose process-level cause-and-effect patterns. Because the business pain has been identified, there will be a strong desire to address it.

Related Posts

FREE 18+ Audit Checklist Templates in PDF MS Word | Excel ...

FREE 10+ Quality Control Checklist Samples [ Welding, Inspection ...

FREE 10+ Warehouse Management Samples in PDF DOC

FREE 10+ Management Checklist Samples in PDF MS Word ...

FREE 8+ Project Audit Report Samples in PDF

FREE 3+ Food Safety Audit Checklist Samples [ Internal ...

FREE 10+ Facilities Management Report Samples in PDF MS Word

FREE 16+ HR Audit Report Templates in PDF Google Docs | MS ...

FREE 5+ Brand Management Report Samples in PDF DOC

FREE 5+ Audit Program Templates in MS Word PDF

FREE 12+ Information Technology Audit Report Samples ...

FREE 11+ Risk Management Report Samples in PDF MS Word

FREE 9+ Internal Audit Checklist Samples [ Financial, Company, HR ...

FREE 14+ Data Audit Report Samples & Templates in PDF

FREE 8+ Access Audit Report Samples in PDF MS Word